In this paper, jointly produced by the United Nations Industrial Development Organization (UNIDO) and the Leadership Group for Industry Transition (LeadIT), we provide an overview of the key components of green public procurement (GPP) policy design and methodologies for target setting. We aim for this study to be a “how to guide”. To do this, we provide evidence on the role GPP can play in accelerating emissions reductions from harder to abate sectors with a focus on steel, cement and concrete, demonstrate national best practices, and explore the impact of a regional or global GPP procurement program on demand creation for low carbon products and materials.

This study provides a background to the Industrial Deep Decarbonization Initiative (IDDI). The initiative is coordinated by UNIDO and brings together a strong coalition of private sector partners and multilateral organizations, including Mission Possible Platform, LeadIT, IRENA and the World Bank.

The need for industry decarbonization is nothing short of critical.

Global momentum for deep decarbonization of harder to abate industries (including steel, cement, aluminum, chemicals, plastics, metals and mining, aviation, and heavy-duty transport) is growing. This is the next frontier in climate mitigation, as these heavy industry activities are energy-intensive and typically rely on fossil fuel inputs, giving rise to significant CO2 emissions. Emissions from the production of five basic industrial materials – steel, cement, plastic (and other chemicals), paper and aluminium – account for 20% of global CO2 emissions and demand for these materials is only expected to increase as many countries around the world continue to industrialize. Therefore, there is growing awareness that emissions from heavy industry must be reduced sharply in order for the world to reach the target of the Paris Agreement: to limit global warming to “well below” 2 degrees Celsius.

These five heavy industry sectors are harder to abate.

Discussions on how to decarbonize heavy industry typically revolve around four interrelated solutions: decarbonizing all energy inputs, increasing energy efficiency, reducing process emissions, and promoting material circularity. For many industries, energy inputs are the main source of emissions. Energy efficiency solutions, such as better insulation and using waste heat, can help to reduce the process energy demand. The Energy Transitions Commission estimates that energy efficiency could be improved by about 30%, either through the latest generation of industrial processes or through completely new processes. However, in some industries, such as cement, steel and chemicals, efforts will also be needed to reduce process emissions that arise during the conversion of raw materials into intermediate or final products. For example, process emissions account for almost two-thirds of the total emissions from cement production. Preventing these emissions requires significant shifts in production processes. In steelmaking this could be done via the use of electric arc furnaces or direct reduction of iron with renewably produced hydrogen instead of coking coal. In cement production this could be through using alternative binding agents or carbon capture and storage (CCS) technology. Lastly, material circularity can help to reduce the demand for brand new industrial products and, in turn, make decarbonizing the production process less of a challenge. However, even in a scenario with increased circular economy, over one billion tonnes per annum of newly produced steel will be needed globally by 2050.

Industry transition requires public policy support.

The four solutions detailed above entail a transition away from current carbon-intensive patterns of industrial activity and rely significantly on the diffusion of low-carbon innovations into existing industrial systems. Some of the technological and process innovations that form part of these solutions are commercially viable or in pilot stages. Others still require considerable research and development. Some innovations may be incremental – such as energy efficiency solutions – and others may be more radical. Either way, significant policy support is fundamental to de-risking the investments in the development, commercialization and deployment of these innovations, which are estimated to cost $25 to $60 USD per tonne CO2 for steel and $110 to $130 USD per tonne CO2 for cement. De-risking can be achieved by supporting the development of lead markets and catalyzing demand for green industrial products.

Green public procurement is a policy tool gaining a lot of attention.

Governmental expenditure on works, goods and services is estimated to represent 14% of GDP in the EU and up to 30% of GDP in developing countries, giving public procurement a colossal purchasing power. As public procurement of infrastructure such as buildings and bridges is often significant, the introduction of GPP policies could stimulate the demand for low carbon concrete and steel products. With GPP, public authorities use their purchasing power to procure goods and services with reduced environmental impact throughout the product life cycle, stimulating the market and rewarding businesses that have developed products and services with lower environmental impacts. Use of GPP to support the development of a market for green commodities is a well-established policy measure in some countries, showing the market producers that there is willingness to pay for the anticipated green premium on these green commodities.

- GPP can cover a wide range of carbon-intensive products and large infrastructure, such as roads, buildings and railways, public transport, and energy. In particular, government construction projects can be substantial in size, offering significant opportunity for GPP measures to reduce emissions from construction (including in steel and cement production).

- GPP policies can take several forms. For instance, governments may impose minimum requirement regulations or preferential buying obligations for low and zero carbon steel and cement, subject to a certain greenhouse gas (GHG) emissions benchmark. Alternatively, GPP can be employed on a voluntary basis or combined with quotas or restrictions. Additionally, complementary legal quota schemes may be adopted to compel the use of products with zero or lower embodied emissions or restrict products with high carbon footprints.

- A procurement alliance between a coalition of countries may be more successful in catalysing large- scale demand for green products and in addressing international competitiveness issues when compared to countries with separate GPP standards. Given the regional and global nature of many heavy industry value chains, GPP policies in a single nation may be insufficient to catalyse transformation across the sector. An industry transition procurement alliance could overcome this challenge but would require significant effort. Such a shared approach would need agreement over, and standardization of, terminologies, GHG emissions calculation methods, minimum standards, as well as processes for the allocation of certificates, monitoring, reporting, verification and compliance mechanisms.

There are many ways to design a GPP policy.

In this brief study, jointly produced by the United Nations Industrial Development Organization (UNIDO) and the Leadership Group for Industry Transition (LeadIT), we provide an overview of the key components of GPP policy design and methodologies for target setting. We aim for this study to be a “how to guide”. To do this, we provide evidence on the role GPP can play in accelerating emissions reductions from harder to abate sectors with a focus on steel, cement and concrete, demonstrate national best practices, and explore the impact of a regional or global GPP procurement program on demand creation for low carbon products and materials.

This study provides a background to the Industrial Deep Decarbonization Initiative (IDDI).

Under the leadership of the UK and India and participation of other countries, including Canada and Germany, the 12th meeting of the Clean Energy Ministerial will witness the launch of a new Industrial Deep Decarbonization Initiative. The initiative is coordinated by UNIDO and brings together a strong coalition of private sector partners and multilateral organizations, including Mission Possible Platform, LeadIT, IRENA and the World Bank. The IDDI aims to stimulate demand for low carbon industrial materials, like ‘green’ steel and cement, which are two of the most carbon intensive commodities on the planet. The initiative will work with governments worldwide to standardize a life cycle assessment of embodied carbon, set ambitious procurement targets and establish tools for comparing the environmental impact of industrial products. TheIDDI will also host a campaign that enables unprecedented public policy making on market creation of low carbon industrial materials and generates commitments in one of the next frontiers in the race against climate change. Together, the stakeholders and governments involved in the IDDI are encouraging much needed public and private purchasing commitments in decarbonised steel and cement, and subsequent investment into product development.

The expandable sections take a more detailed look at the GPP policy design, target setting, potential impact and co-benefits.

GPP Policy Design: A “How to” Guide for Steel & Cement Sectors

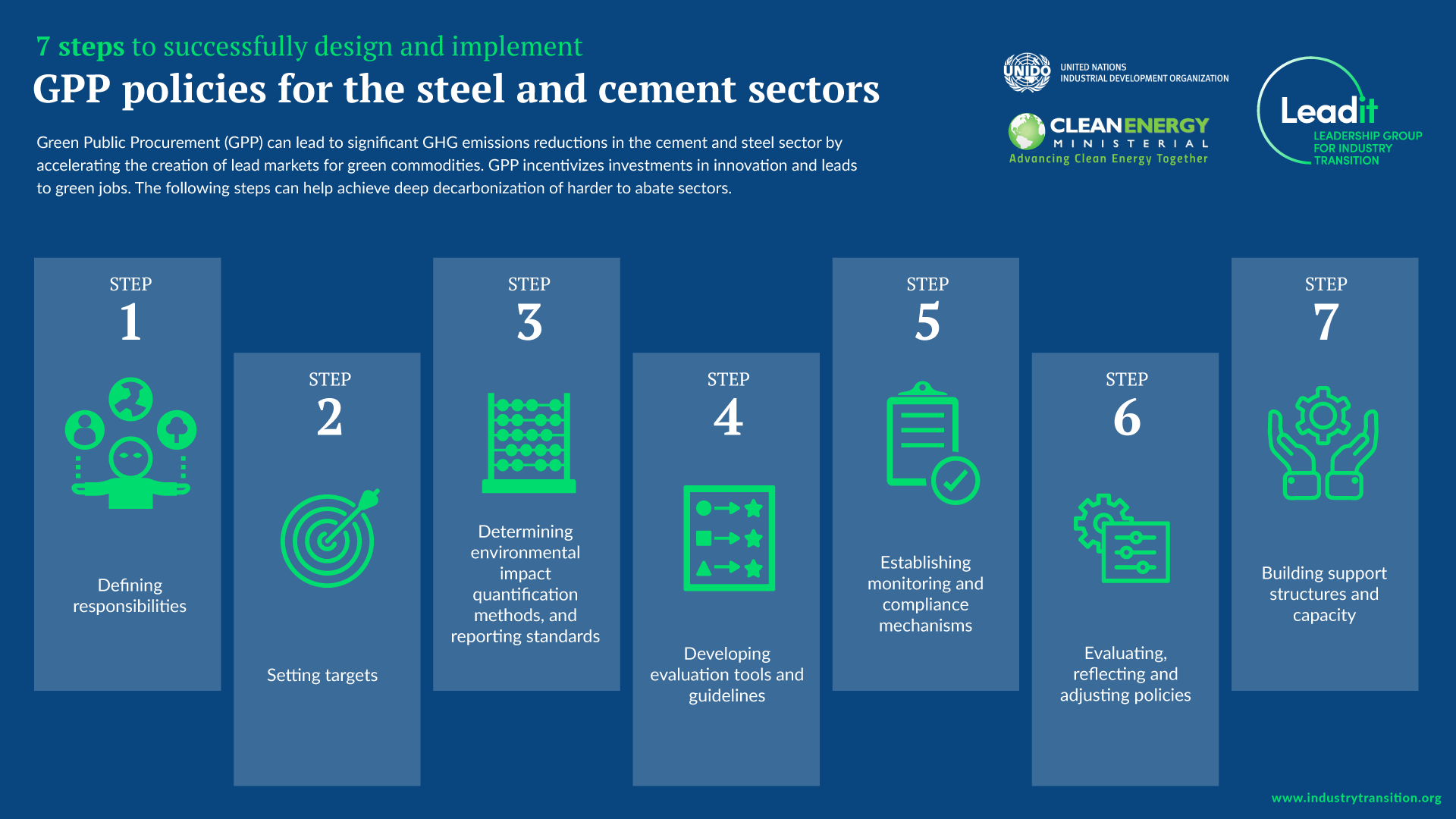

We have identified the following steps to successfully design and Implement GPP policies aimed at deep decarbonization of harder to abate sectors such as steel and cement.

Step 1. Defining responsibilities

Firstly, it needs to be established who is responsible for the design, implementation and monitoring of GPP policies for steel and cement sectors across agencies. This is important because procuring agencies are typically spread across government func- tions and regional levels.

The design of GPP policies, such as national objectives, covering sectors and man- dates is often done at national level by a ministry or the National Procurement Agency. For example, the Government of Canada Policy on Green Procurement was developed by the Agency for Public Service and Procurement of Canada and is now managed by the Treasury Board of Canada Secretariat’s Centre for Greening Government. It sets out GPP requirements and objectives and holds deputy heads responsible for the implementation and realization of the objectives. They are responsible for integrating environmental stewardship into procurement practices, setting GPP targets tailored to reflect mandates, establishing management processes, ensuring key staff are trained, and monitoring and reporting annually on GPP performance. In the UK, the Government Buying Standards (GBS) were created by the Department for Environment, Food & Rural Affairs and the Cabinet Office. This government department set out the minimum mandatory GBS that UK Government departments and their related organizations have to meet.

More specifically, GPP target development requires consultation with industry and environment experts. Many countries follow a similar process of drafting a proposal and going through several rounds of stakeholder consultation. For example, in the EU, the Joint Research Centre (JRC) drafts a report broadly surveying public procurement within a sector and introduces quantitative targets. Three rounds of feedback are incorporated, the first two being working groups open to all interested parties and the third being a written stakeholder consultation. The targets then go through an inter-service consul- tation within the EU Commission before they are published. Similarly in Japan, the Ministry of Environment develops and revises a basic policy through consultation with review committees consisting of academics, technical experts and industry stakeholders. Then, public institutions set their own targets through reference to the basic policy and submit reports annually on implementation to the Ministery.

To enable monitoring of the effectiveness of GPP policies across procuring agencies, a central body can gather reports by the various procuring agencies.

Recommendations

- Use a collaborative target-setting process that includes stakeholder consultation before policies are ratified. The involvement of industry experts in choosing quantitative targets ensures that it Is feasible for industry to meet the targets.

- Create a central body responsible for the design, support and monitoring of GPP policies, and establish responsibilities regarding the implementation of policies.

Step 2. Setting targets

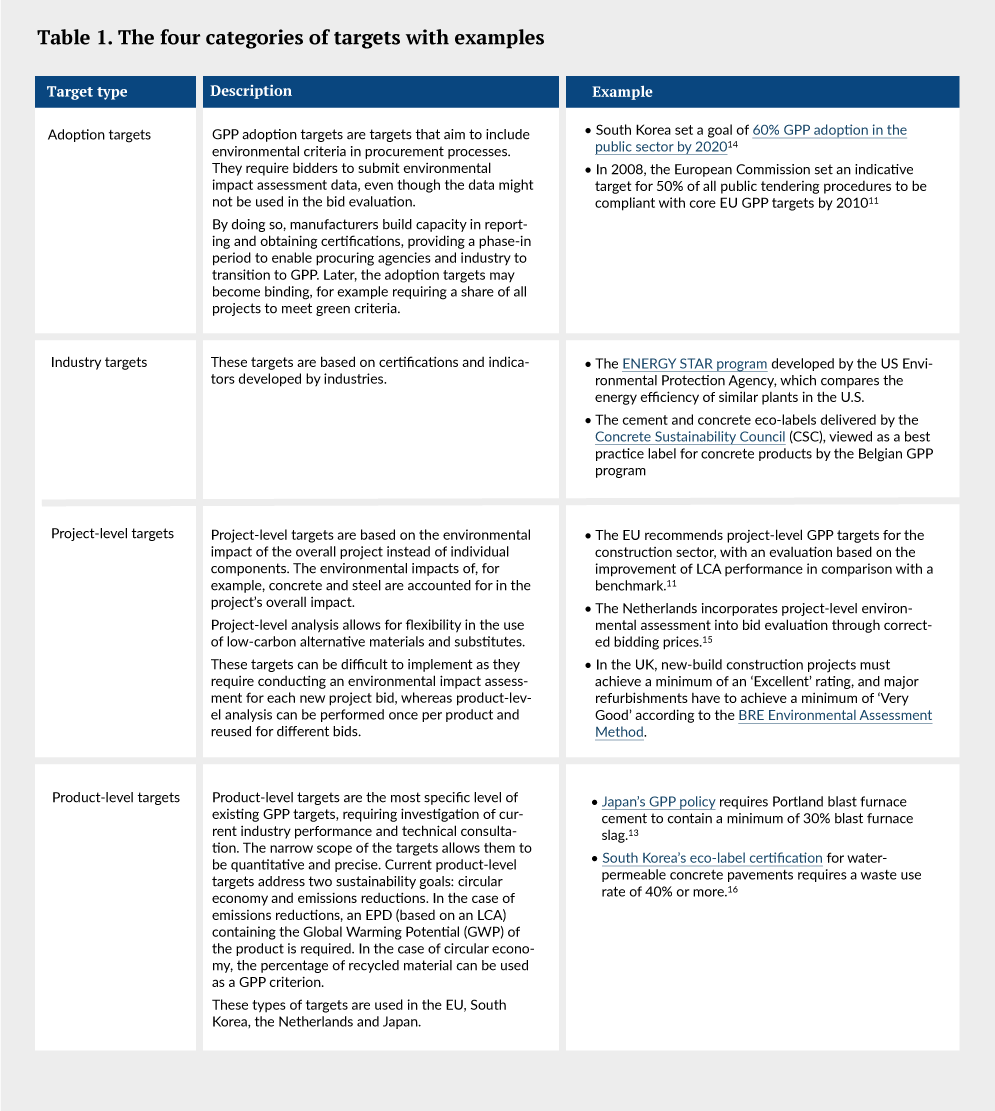

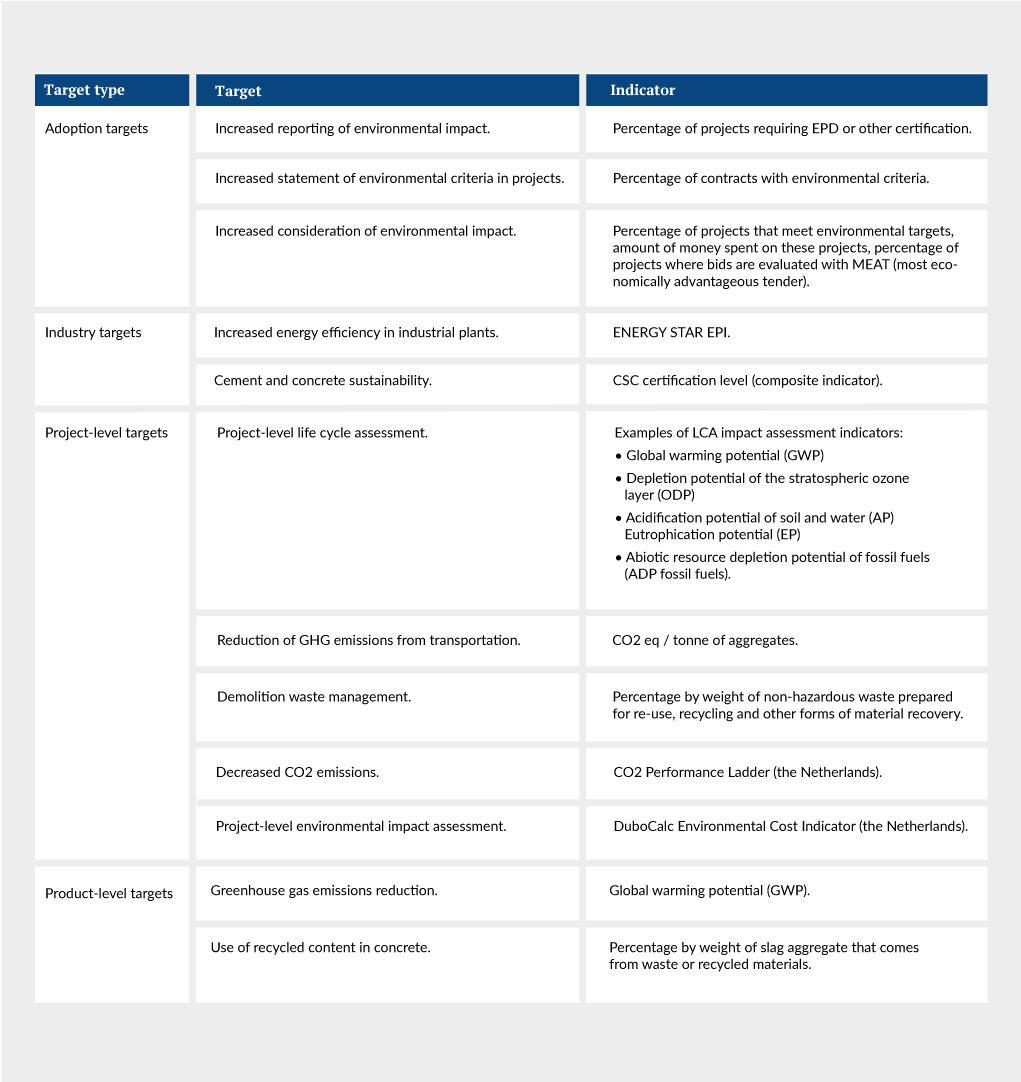

For a successful implementation of GPP programs, clear quantitative targets are needed. There are four categories of GPP targets: adoption targets, industry-level targets, project-level targets, and product-level targets (detailed in Table 1 below). A summary of key GPP aspects in selected countries is in Annex 1, and a more extensive list of detailed examples of targets can be found in Annex 2.

Three main aspects should be considered when setting targets:

1. Voluntary or required

When using voluntary targets, the consideration of environmental criteria does not guarantee that it will be included in the GPP bid evaluation. With required targets, targets can be either minimum requirements (mandatory criteria) or preference-based (performance criteria). Mandatory criteria disqualifies tenders that do not meet the minimum requirements. Performance criteria do not disqualify bids but give preference in the evaluation. They are only effective if environmental impact has a large enough effect on the final decision to compete with other factors, such as price. Currently, performance criteria tend to be project-level, while mandatory criteria tend to be product-specific.

2. Project- or product-level

Product-level targets use product-specific environmental assessments (e.g., EPDs) which can be created once and reused for multiple tenders. For project-level tar- gets, an environmental impact analysis must be performed for each bid, making project-level targets more complex to implement. However, they encourage material efficiency, circular economy and in the use of low-carbon alternative materials, which product-specific targets do not incentivize.

3. Internal or external to industry

Targets based on industry average can disqualify the worst polluters from bidding,

but they are likely to promote existing best practices rather than promote further innovations to reduce emissions. Targets that are set externally must promote industrial efficiency without barring too many companies from bidding. Targets could be adjusted annually, for example reducing the maximum global warming potential (GWP) limit incrementally to achieve net-zero by 2050.

Recommendations

To disqualify worst polluters and incentivize break-through innovation, a two-pronged approach to setting targets is recommended:

- Minimum product-level targets must be met for the bid to be considered, thereby encouraging the adoption of existing green practices. Minimum product-level requirements such as maximum acceptable GWP limits are recommended.

- Project-level performance targets reward bidders with best-in-class materials efficiency, thereby inducing innovation. They can be used for project-level bid evaluation to give preference to tenderers that exceed the minimum requirements. The weight of environmental criteria must be significant compared to other criteria such as price for this to have an impact on the final decision.

Step 3. Determining environmental impact quantification methods and reporting standards

Reporting standards and methods to determine and evaluate the environmental footprint of a product are crucial for the purchasing authority’s decision-making process.

The most commonly accepted method to quantify embodied emissions in construction materials is life cycle assessment (LCA). It is a framework following the ISO Standard 14040 in which the environmental impacts of all materials within the specified scope are calculated.

The most common reporting method used to communicate the results of LCAs in a standard format is environmental product declaration (EPD). The EPDs follow guide- lines specific to certain products called product category rules (PCR). These rules specify the unit of measurement, system boundaries and assumptions to be made, making EPDs transparent and comparable in order to be able to easily identify the most environmentally friendly option. Currently, there are over 130 PCR available on the International EPD System’s website. PCR are developed through participatory stakeholder processes by companies and organizations or institutions involving LCA experts. EPDs contain multiple indicators, including global warming potential (GWP) which is an indicator of embodied emissions. The more specific the data (facility and supply chain-specific primary data), the more accurate the EPD will be for a specific product from a specific manufacturing facility. EPDs have been adopted in GPP pro- grams, such as the Californian “Buy Clean” and EU GPP targets.

The other reporting standard is eco-labels. These labels are certifications awarded to products when they fulfil a set of performance criteria, such as ResponsibleSteel for steel and the Concrete Sustainability Council certification for cement. Eco-labels do not offer a way to differentiate between products that simply meet the minimum requirements and those that go and above and beyond the criteria requirements and therefore may not incentivize breakthrough innovations. Another drawback is that many countries have created their own eco-labels, making harmonization across countries difficult. Eco-labels are simple to use as they collapse many measurements across a range of criteria into a single indicator. However, they can obscure details and can be a drawback when the contractor wants to minimize a specific indicator, such as global warming potential, as this information is not provided by the eco-label. Furthermore, eco-labels do not provide a specific measurement of impacts achieved through their application.

For example, German procurement guidelines take into account whether products have the German environmental label ‘Blauer Engel’, or, for products where this does not exist, the European environmental label. Another example is the CO2 Performance Ladder developed by the Netherlands to certify tenders that have taken measures to limit a company’s CO2 emissions. The submitted project price is adjusted based on the CO2 Performance Ladder level with a deduction of 1% off the submitted price per level.

Once a reporting standard for specific goods and materials has been established by a GPP implementation body, the process of compiling a database of products can streamline product evaluation and increase transparency. This enables information sharing across procurement agencies and makes it easier for procurement officers to access environmental information for products.

Recommendations

- EPDs are the reporting format recommended by many GPP experts, since they are standardized across geographies and contain very comprehensive information. However, they can be complex and costly.

- The use of eco-labels could be made more effective in some jurisdictions where an established eco-label Is also being used by industry for products covered by GPP.

- Compiling an open-access database of products can help streamline product evaluation and increase transparency.

Step 4. Developing evaluation tools and guidelines

To ensure transparency and fairness in bid evaluations, standardized bid evaluations methods can be designed and implemented through tools and guidelines.

First, GPP policies need to state, through official guidelines, which environmental documents are required from bidders and how procuring agencies will incorporate environmental criteria into bid evaluation. For example, the policy could require pro- curers to use the most economically advantageous tender (MEAT) approach with price discounting, as adopted in the Netherlands.

Software tools are an especially valuable way to share GPP program guidelines as they can disseminate the most up to date GPP targets, while simplifying the procurement process. Examples of existing evaluation software include:

- KONEPS (South Korea), a fully integrated procurement system, which manages the creation of procurement requests, tendering, contracting, payment and reporting.

- MVI (the Netherlands), an online tool created by the Netherlands to create tender documents with environmental criteria.

- DuboCalc (the Netherlands), a publicly accessible evaluation software based on LCA that computes the environmental cost of a project and converts it into an environmental cost indicator value. This value can be used as a minimum require- ment or lead to a price discount.

- BM (Sweden), a calculation tool for building projects based on LCA methods, sim- plifying environmental impact calculation.

Recommendations

- Develop official guidelines for reporting and evaluation that ensures the transparency and fairness bid of evaluations.

- Software tools can help GPP policy bodies to streamline GPP implementation, as it can automatically disseminate new GPP targets and facilitate the bid evaluation work.

Step 5. Establishing monitoring and compliance mechanisms

In order to implement GPP policies in a rigorous way, ensuring fairness to the tenderers, GPP programs must base targets on harmonized standards which are verified by third parties.

Monitoring requires clear measurement and verification protocols, including (1) self-reported data from the tenderer, (2) spot checks by technical authorities, and (3) third-party verification. Today, few countries have clearly defined policies for measurement and verification due to the technical complexity of monitoring emissions along the supply chain, especially for large-scale projects involving several suppliers and subcontractors. The EU’s GPP targets define verification protocols for each criterion, some of which require monitoring performance as the construction progresses.

Enforcement protocols are needed in the case of contractors who do not meet their environmental obligations. Recourse may be required in the form of rebuilding, fines against the contractor and/or project cancellation. An example of this in current GPP practice can be found in the Netherlands, where a contractor must pay a penalty that is 1.5 times the original price discount if the project does not meet the environmental performance proposed in the bid. A legal framework may be necessary to enable litigation against negligent actors.

Recommendations

- Define a measurement protocol in the contract to verify that the proposed environmental impact reductions are met.

- Create a policy for enforcement that outlines legal recourse when tenderers do not perform as promised.

Step 6. Evaluating, reflecting and adjusting policies

To evaluate the efficacy of the GPP policies in reducing GHG emissions and how they can be improved over time, an effective process for collecting feedback and data should be created.

In Japan and South Korea, procuring agencies report their purchases to a central body annually. This office compiles the data and estimates the GHG emissions reduction using the share of green products purchased and the difference between the average emissions of a green product and a conventional one. In Sweden, a procurement agency was created in 2015 to support and monitor public procurements across the country. They develop guidelines and criteria now in use through procuring entities. In Canada, the Policy on Green Procurement requires departments to report on green procurement, and the policy is evaluated through the annual Departmental Sustainable Development Report.

GPP targets can be reviewed regularly to adjust targets over time as technological advancements are made. This ensures that GPP is continually promoting green innovation. For example, Canada’s Greening Government Strategy is reviewed by Cabinet every three years to report on progress and to propose improvements. Two models are possible for the rate of change, as proposed by the Carbon Leadership Forum. The first is a percentage reduction from the initial value to reach zero-carbon by 2050. The second is continually setting the value based on industry performance, such as the 80th percentile of industry performance.

Recommendations

- Create a central body that estimates the overall impact of GPP policy on GHG emissions. This central body may receive reports from all government agencies with aggregate purchases made annually.

- Review, on a two- to three-year basis, targets that have been set to lower the maximum acceptable GWP limits. With the initial value as a baseline, adjust the limit to reach net-zero.

Step 7. Building support structures and capacity

While not strictly necessary, support structure can help improve the implementation of the GPP policy. Here are four recommended actions that can be combined with GPP policy design:

- Education and capacity building through training programs, guidebooks or a GPP agency responsible for providing supporting information can teach procurement officers how to draft tender documents with environmental criteria and incorpo- rate life cycle impacts into bid evaluation.

- Investment in clean manufacturing through deployment of renewables, improved energy storage and electricity grid modernization has downstream effects for harder to abate industries. In addition, public investment in research and development of carbon capture and sequestration, electrification of heat, and transformation of low-carbon technologies will be needed to enable breakthrough innovations.

- Loans, grants and financial support programs can be created for capital-con- strained small and medium-sized enterprises (SMEs). This will help SMEs overcome the switching costs associated with retrofitting industrial facilities and retraining workforces.

- Financial incentives can be offered to procurement agencies to promote GPP program adoption. For example, local governments in South Korea with high performance in GPP implementation are awarded a larger budget and public insti- tutions receive a performance bonus.

GPP potential for reducing GHG emissions

Key take-aways

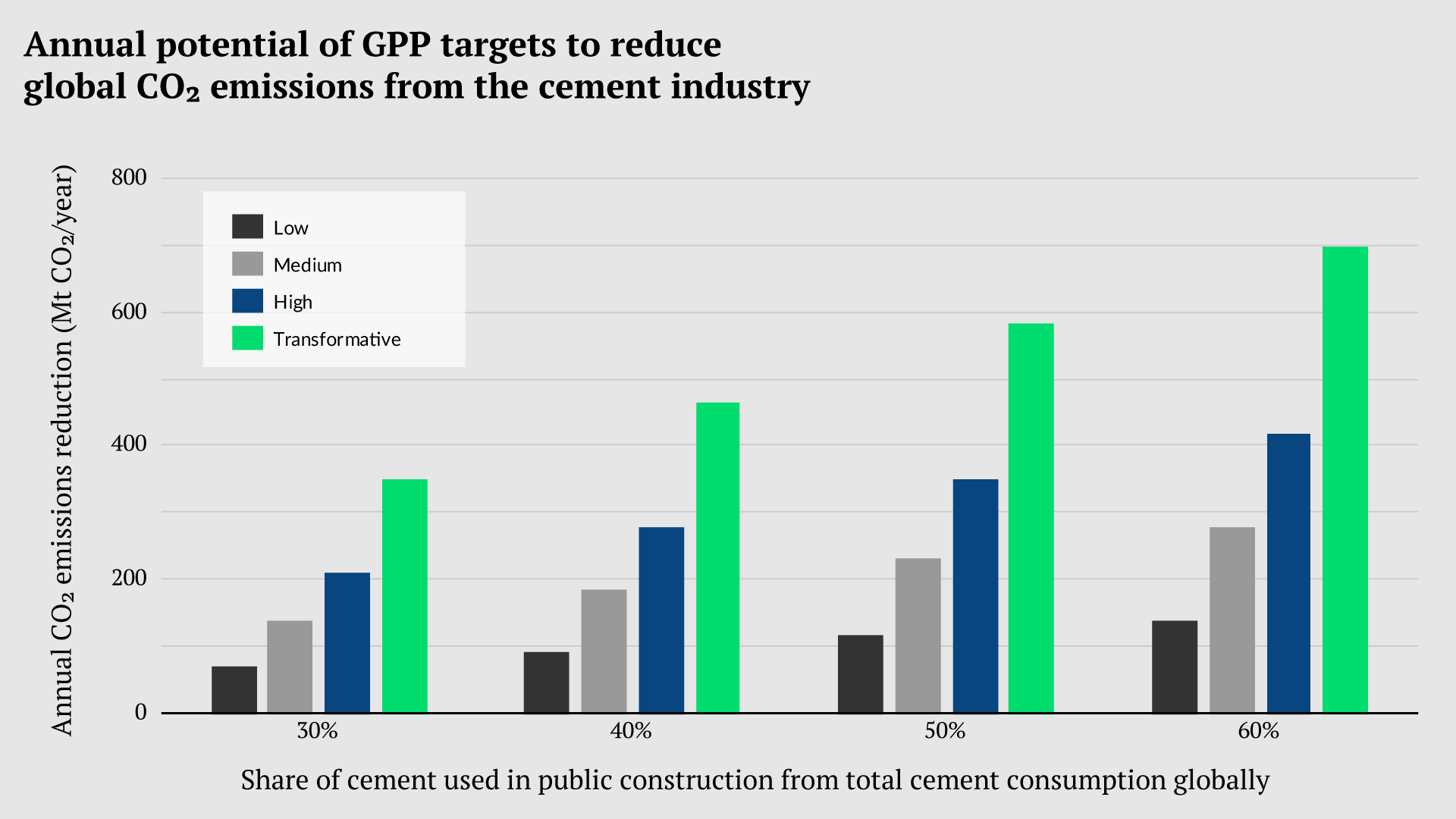

- Assuming around 40% of cement is used for public constructions globally, GPP with a 10%, 30% or 50% reduction target in cement CO2 intensity can result in an annual CO2 emissions reduction of 93, 280 and 470 million tonnes of CO2 (Mt CO2), respectively.

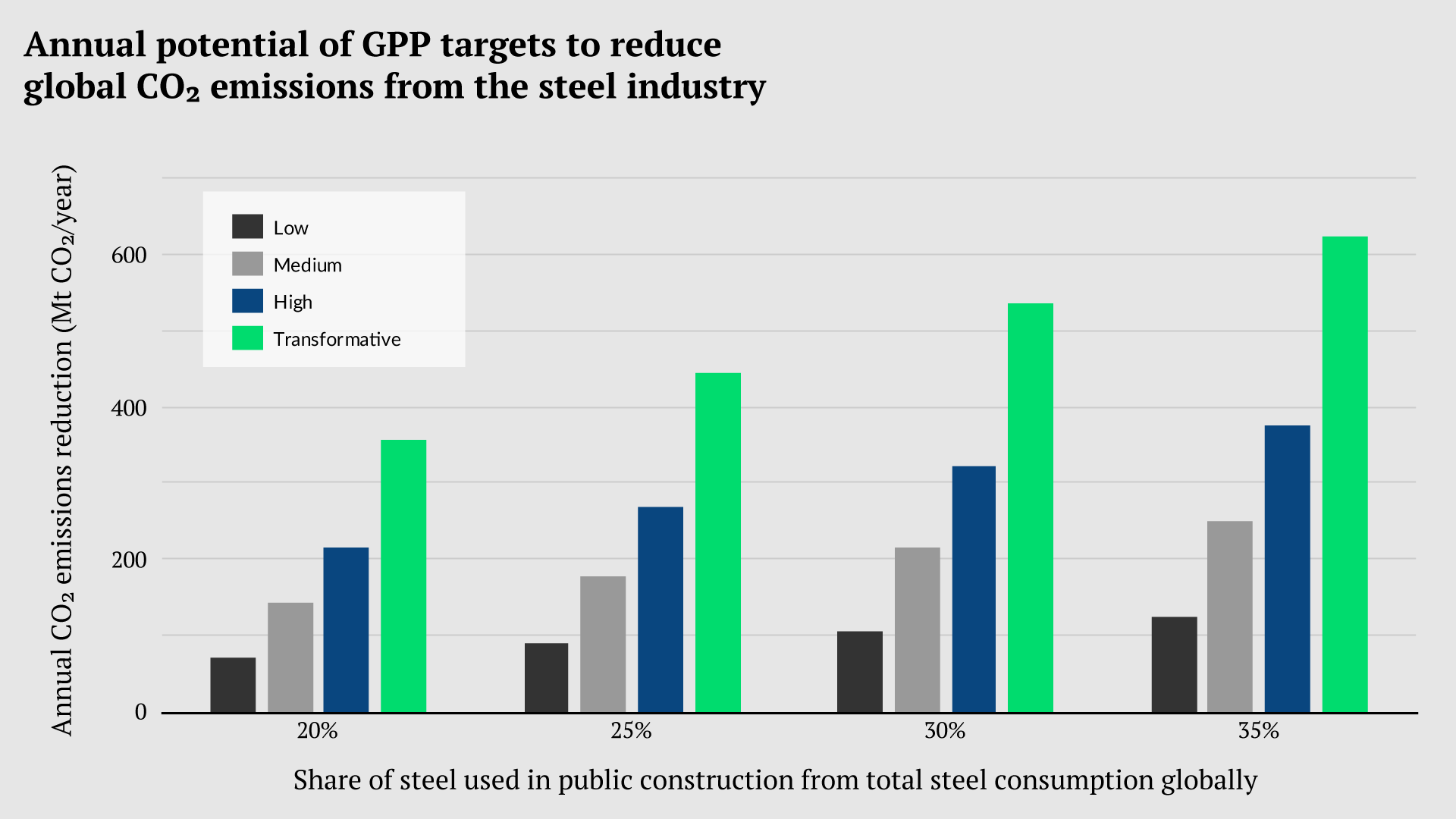

- Assuming around 25% of steel is used for public constructions globally, GPP with a 10%, 30% or 50% reduction target in steel CO2 intensity can result in an annual CO2 emissions reduction of 90, 270, and 450 million tonnes of CO2 (Mt CO2), respectively.

- Since about 80% of cement and 90% of steel is manufactured in the top 10 producing countries, respectively, the adoption of GPP in only a limited number of countries can help to achieve the majority of the GHG emissions reduction potential.

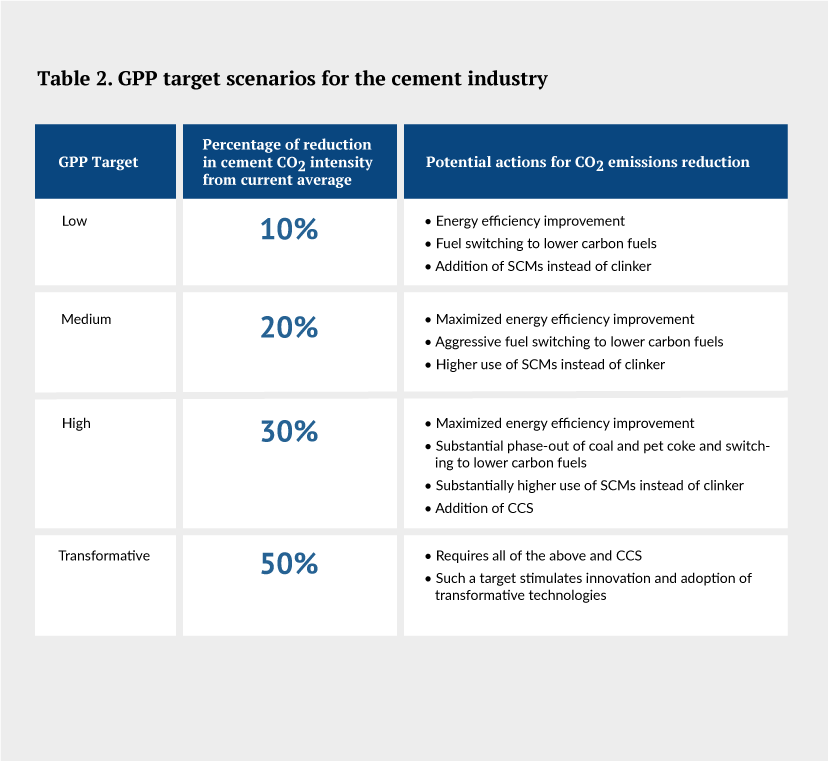

Scenarios for the cement industry

We developed scenarios for GPP targets for the CO2 intensity of cement production (Table 2). In addition, we estimated the GPP impact on GHG emissions reductions

for several different scenarios, taking into account the different shares of public construction from total cement consumption. The scenarios were developed for global levels, with the acknowledgment that specific countries and production plants differ. The scenarios are in line with data points collected for the U.S., Canada, the UK and Germany. As a reference point, public procurement accounts for 46% of cement consumption in the United States. The results of our analysis are shown in Figure 1. To put the GHG emissions reduction potential results into context, in 2019, total GHG emissions in the UK were about 454.8 MtCO2-eq.

Scenarios for the steel industry

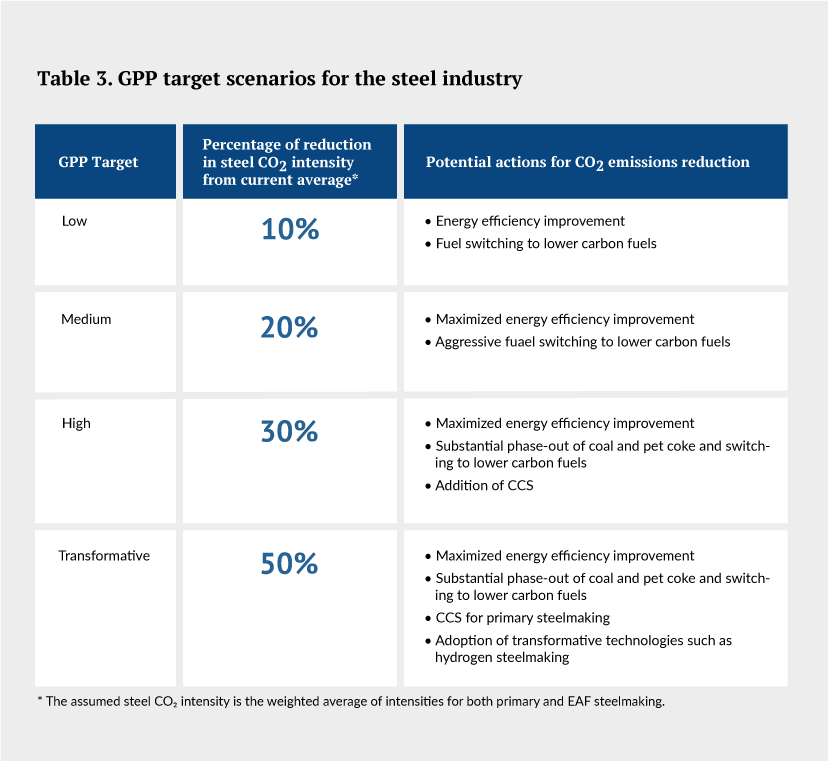

There are four scenarios, with various GPP targets for CO2 intensity of steel, that could be set by GPP programs (Table 3). For reference, public procurement of steel represents 18% and 32% of steel consumption in the U.S. and Germany. The reduction percentage in steel CO2 intensity from current average assumes weighted average of intensities for both primary and EAF steelmaking. In some countries with a high share of primary steelmaking, simply switching from primary steelmaking to EAF steelmaking can help

to achieve some of the GPP targets. But given the limited availability of scrap, the high capital cost of switching to different production process (while existing assets might not be at the end of their lifetime) and several other reasons, switching to EAF may be more challenging. Therefore, other measures, such as energy efficiency, fuel switching and CCS are also considered. For more aggressive reduction, the adoption of transformative technologies, such as hydrogen steelmaking using direct reduced iron (DRI) or electrolysis of iron ore, are other promising technological paths.

GPP co-benefits for society and the environment

There are multiple benefits to GPP, with positive environmental, socio-economic and political effects that go beyond the specific purchase:

- Socio-economically, it incentivizes producers to invest in developing green technologies, enhancing marketing potential, innovation, sales, and export. Such Initiatives ultimately help trigger broader socio-economic growth by creating green jobs across value chains.

- Environmentally, GPP allows public authorities to achieve their environmental goals by effectively reducing GHG emissions, local air pollution and waste while promoting energy and resource efficiency. Furthermore, GPP sets an example for private procurement, demonstrating what is possible and popularizing green products already on the market.

- Finally, politically, GPP enables public authorities to demonstrate their commitment to the race to net-zero through concrete measures, supporting transition of the harder to abate sectors.

A call for harmonization across countries

GPP policies need to be harmonized across countries to avoid the potential distortion of a single market. This would also help GPP policies to simplify their implementation and encourage competition in green innovations across borders. Standardized environmental reporting methods, such as EPDs, would give countries a shared language to communicate about GPP, while also simplifying the task for bidders. In addition, an international harmonization process would enable countries to share the cost of defining targets and create frameworks and tools through consultation of technical experts and industry stakeholders. Creating this process would also help build the shared capacity of trained professionals who are then able to transfer knowledge and expertise across borders.

GPP policy components that are recommended to be established internationally are (1) a list of eligible products, and (2) feasible while ambitious minimum requirements for each product. Furthermore, standardized calculation and reporting methods for embodied emissions and other environmental impacts, such as LCAs and EPDs, need to be agreed upon internationally.

Other components of GPP policy can be compatible but do not need to be equivalent. For example, some countries may choose to set more ambitious GPP targets than the harmonized minimum requirements. Others may establish new tools for bid evaluation, financial incentives or emissions reduction monitoring and verification. Individual countries’ experimentation provides new examples of GPP best practices that can inspire improvements from others. The Netherlands’ work illustrates this, as they choose to follow the EU GPP targets with additions, such as price discounting and bid evaluation software.

Conclusion

Public procurement accounts for a significant share of the international economy. Governments are increasingly using their purchasing power to drive industry towards more sustainable products and materials through green public procurement programs. By creating lead markets for green commodities, GPP can lead to significant GHG emissions reductions in the cement and steel sectors. Given that about 80% of cement and 90% of steel is produced in the top 10 producing countries, the adoption of GPP only in limited number of countries can help to achieve majority of the GHG emissions reduction potential. Additionally, GPP can make manufacturing more globally competitive and create high-paying jobs. Sound GPP policy design would ensure that countries capture all the positive co-benefits that green public procurement can provide.

Information received from several countries shows that the most challenging barriers to GPP implementation for steel, cement and concrete are (1) the lack of high resolution data across full supply chains, (2) the lack of standardized, comprehensive calculation methods for reporting and comparing a product or a project’s environmental impact that take into account aspects such as fuel switch and optimization of material usage and (3) the lack of procedures and knowledge to apply and report on environmental requirements.

These insights confirm the need for a green public procurement alliance that brings together countries’ private sector partners and multilateral organizations to address these barriers in a concerted manner. The Industrial Deep Decarbonization Initiative will work to develop and standardize data collection mechanisms and environmental assessment methods, establish ambitious procurement targets and design tools for comparing the environmental impact of industrial products. Working through an alliance has the potential to catalyze industrial transitions in the harder to abate sectors of steel and cement, in which decarbonization Is key to the race to net-zero.

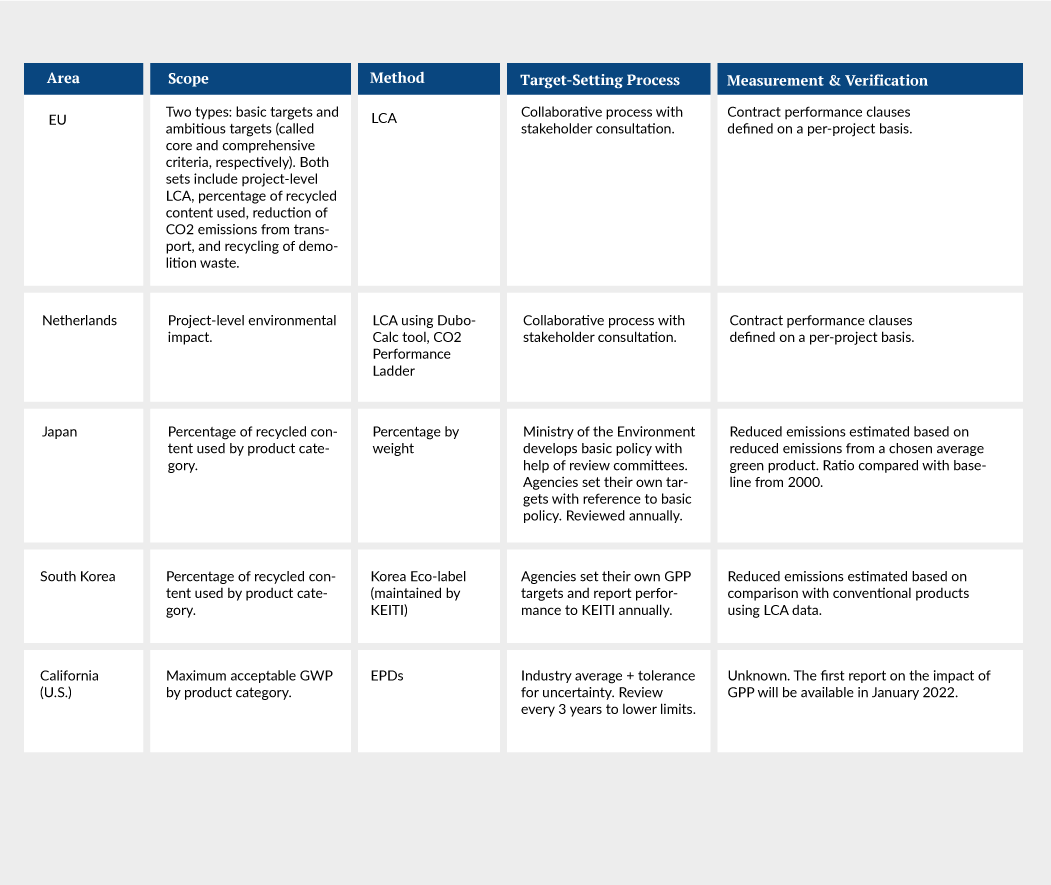

Annex 1: Summary of aspects of GPP target setting in selected countries or regions

Annex 2: Target types with examples

Acknowledgements

This report was made possible by support from the UK Department for Business Energy and Industrial Strategy (BEIS). The authors would like to thank Rana Ghoneim, UNIDO, Mateus Mendonça Oliveira from UK BEIS, Jan Kiso, Industry Division of

the German Federal Ministry of Economic Affairs and Energy, Matthew Pelletier

and Soledad Reeve, Treasury Board Secretariat of Canada, Marta Berglund from the Swedish Ministry of Environment, and Francisco Pereira from the Mission Possible Partnership for their valuable input to this study and/or their insightful comments on the earlier version of this document.

Disclaimer

The authors and their affiliated organizations have provided the information in this publication for informational purposes only. Although great care has been taken to maintain the accuracy of the information collected and presented, the authors and their affiliated organizations do not make any express or implied warranty concerning such information. Any estimates contained in the publication reflect authors’ current analyses and expectations based on available data and information. Any reference to a specific commercial product, process or service by trade name, trademark, manufacturer, or otherwise, does not constitute or imply an endorsement, recommendation or favouring by the authors and their affiliated organizations. This publication report does not necessarily reflect the politics or intentions of the contributors.

This document may be freely quoted or reprinted, but acknowledgment is required.