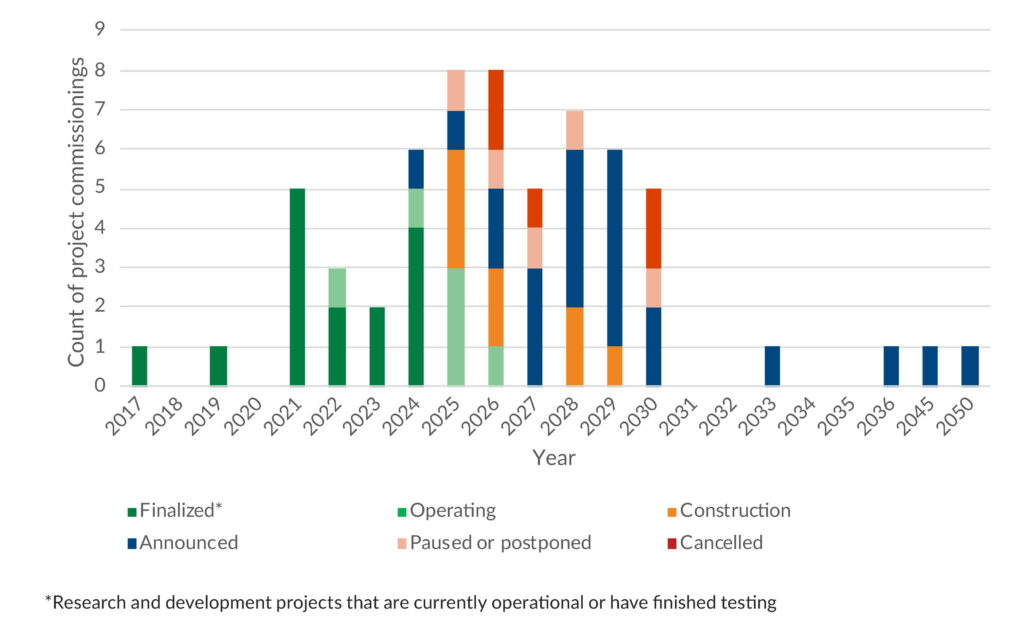

After several years of growing optimism, the global green steel and green iron sector is entering a pivotal moment. Momentum slowed in 2025, with new project announcements captured in the green steel tacker falling from a peak of 15 projects in 2021 to just two in 2025. Planned primary green steel production capacity for 2050 currently represents less than 2% of today’s total global steel production.

Despite the slowdown in announcements, 2026 is set to be a decisive year for delivery. The tracker identifies Stegra’s Boden project in Sweden as the most significant near-term milestone in 2026. It represents the first potential full-scale commercial commissioning of green steel. Several pilot and demonstration projects are also scheduled to advance this year, including in Germany and the United States.

Successful commissioning of Stegra in Boden in 2026 and the roll-out of the longer-term projects in the Hybrit alliance of SSAB, LKAB and Vattenfall, alongside pilot projects globally, will impact the sector in the coming years. These projects will influence confidence and the pace of transition not just in Sweden and not just in steel production, but internationally and across industry in the coming years.

Per Andersson

Head of Secretariat, LeadIT

However, the green steel tracker shows that delays are common among projects with publicly reported commissioning dates, while limited transparency makes it difficult to assess timelines for many others. In 2025, several high-profile projects, particularly in Europe, were paused or cancelled.

Project status by planned commissioning year, global (source: Green Steel Tracker)

Planned capacity gap

LeadIT’s analysis of tracked projects shows that reaching net-zero by 2050 will take many more green steel projects than are planned. We calculate that less than 2% of what is needed is currently publicly announced. At the moment, planned primary green steel capacity by 2050 totals 28 million tonnes per year, alongside 18 million tonnes per year of green iron used as feedstock for steelmaking. These volumes represent only a small fraction of today’s 1 800 million tonnes per year of global steel production, including both primary and scrap-based output. This underscores the scale of ambition still required to decarbonize the sector.

Progress on the ground also remains limited. At present, only around 270 000 tonnes per year of green iron capacity and 60 000 tonnes per year of green steel capacity are operational, meaning only a small share of announced projects has reached production.

The role of policy

Despite falling short of emissions reduction targets so far, incumbent global steelmakers continue to signal commitment to decarbonization, even as they face rising costs, weak demand, and uncertain policy environments. Future policy intervention may prove decisive in sustaining momentum until green steel becomes cost-competitive at scale.

Policy support to get first-of-a-kind green steel projects up and running can deliver benefits far beyond any single plant by accelerating learning, proving the technology at scale, and helping create early markets and confidence across the entire sector.

Aaron Mailtais

Policy Lead, LeadIT

Policy signals to watch

- The start of the EU Carbon Border Adjustment Mechanism’s definitive phase from 1 January 2026 may begin to shape trade and decarbonization decisions, as importers must surrender CBAM certificates priced in line with the EU Emissions Trading System, with effective certificate obligations phased in as free allowances arewithdrawn for EU producers.

- The announcement at COP30 in Belém thatthere will be increased collaboration between certification bodies to align on a global green steel standard or on compatibilities between standards. While still in its early days, this can be a major accelerator for the sector, as it simplifies the process of qualifying a product as being “green steel”.

In summary, meaningful progress is contingent on large, ambitious projects surviving these difficult times, where a combination of declining global steel prices and weak market conditions for European Union steel producers has slowed momentum. Bringing back momentum and confidence could require policy interventions, with 2026 shaping up to be a pivotal year for the steel transition.